Jerome Famularo

Recently, we published a briefing paper that highlights our case against the US Treasury’s Community Development Financial Institutions (CDFI) Fund. The CDFI Fund is essentially a welfare program that subsidizes financial services through tax credits and grants. Congress should eliminate the CDFI Fund because it is a tool for redistributing resources from taxpayers (present and future) to politically favored locations, demographics, and firms.

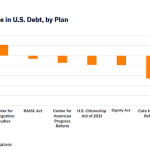

The CDFI Fund recently came under scrutiny after President Trump’s March executive order targeting the Fund with elimination. After that, in May, the White House’s discretionary budget request outlined a net $191 million cut to the Fund’s discretionary funding.

Then, in July, the One Big Beautiful Bill Act indefinitely extended the CDFI Fund’s largest program, the New Markets Tax Credit (NMTC), which was otherwise going to expire in 2025. Most recently, in August, OMB documents showed that the CDFI Fund is not disbursing new funds aside from $35 million for administrative purposes.

The NMTC is the largest program of the CDFI Fund in terms of its fiscal impact, costing the budget over a billion dollars each year. It provides tax credits for a multitude of projects, some of which are highlighted in our briefing paper, in our colleague’s blog post, and in this 2014 report by the late Senator Tom Coburn. These are by no means the only examples of waste, and I invite you to visit the NMTC Coalition’s website and see for yourself.

In addition, the CDFI Fund issues grants to financial institutions to subsidize those firms. Community Development Financial Institutions (CDFIs) can use the grant money to subsidize many facets of their operation, including making loans, shoring up loan loss reserves and capital reserves, and providing development services. Technical assistance grants, meanwhile, are flexible and can be used to purchase equipment, hire consulting or contracting services, pay salaries and benefits, or train staff and board members.

While these grant programs are generally funded through taxpayer dollars, the exception is that some are funded through the Capital Magnet Fund, which is funded by Fannie Mae and Freddie Mac. Ultimately, of course, these Fannie and Freddie fees are passed on to borrowers and investors.

CDFI Fund proponents often point to the program’s popularity and bipartisan support as evidence of its “success.” Naturally, though, programs that enable legislators to take credit for diverting federal funds and tax credits to their jurisdictions are popular with legislators from both parties. Indeed, CDFI Fund grant money is distributed to most counties across the country (see map).

Proponents also claim that CDFI Fund programs are successful at creating jobs and developing communities. But the reality is that to the extent that a CDFI Fund-funded project is “successful,” it is merely redistributing resources from one place to another. For instance, it shifts the tax burden from those who receive grants to non-recipients and from people who receive immediate tax breaks to those who pay taxes in the future.

The CDFI Fund’s own research has found that sustained CDFI lending in a neighborhood did not lead to improved neighborhood conditions. However, many have claimed that NMTC projects have led to jobs. If it is the case that the NMTC creates jobs as its proponents claim, then it must be the case that taxes are a burden on local economies and that cutting taxes is a great way to boost economic activity. Therefore, it makes little sense to limit the tax credit to politically connected firms, causes, and demographics, as the NMTC does.

Of course, a broader tax cut would further increase the national debt, absent a larger spending cut, so even an across-the-board tax cut would merely be “creating” jobs in the present at the expense of future taxpayers unless future spending is cut. Some have claimed that the NMTC pays for itself by increasing tax revenue, but this is a dubious Laffer curve argument. Policymakers should not gamble with taxpayer money.

Proponents also claim that the CDFI Fund grants and tax credits are “leveraged” by private capital. To the extent that the projects do require catalytic public funding, private capital must see them as bad investments. If they’re bad investments, the public funding would be better spent by the taxpayers themselves, and the government already has a litany of other welfare programs designed to redistribute resources to poorer people and neighborhoods. However, to the extent that private capital would be otherwise willing to fund these projects, public funding and tax breaks merely serve as corporate welfare. Therefore, the CDFI Fund acts as either welfare or corporate welfare, depending on the individual project or initiative.

Another claim made by supporters of the CDFI Fund is that it helps improve the economic mobility of residents by investing in poor places. But the best way for people to be economically mobile is to be physically mobile, that is, to move to where the jobs are and get one. Geographical redistribution of resources leads to less efficient outcomes than the free market because it prevents people from engaging in the activities that would best increase their living standards.

In sum, Congress should cut CDFI Fund grants and end the New Markets Tax Credit. Republicans should resist the urge to pivot the CDFI Fund from a patronage network for minority communities to one that favors rural communities. Instead, it makes the most sense to shut down the CDFI Fund completely and stop using taxpayer dollars to subsidize financial services.